United States housing market correction

Encyclopedia

A United States housing market correction is a market correction

or "bubble bursting" of a United States housing bubble

; the most recent began following a national home price peak first identified in July 2006. Because realty trades in illiquid markets relative to financial assets such as common stock, timely valuation lags true values from three months to a year. Certain markets, including San Diego and Detroit, peaked as early as November 2005.

A real estate bubble

is a type of economic bubble

that occurs periodically in local, regional, national or global real estate

markets. A housing bubble is characterized by rapid increases in the valuations

of real property

such as housing

until unsustainable levels are reached relative to incomes, price-to-rent ratios, and other economic indicators of affordability. This in turn is followed by a market correction in which decreases in home prices can result in many owners holding negative equity

, a mortgage

debt higher than the value of the property.

Based on the historic trends in valuations of U.S. housing, many economists and business writers have predicted a market correction, ranging from a few percentage points, to 50% or more from peak values in some markets, and, in spite of the fact that this cooling has not affected all areas of the U.S., some have warned that it could and that the correction would be "nasty" and "severe". Chief economist Mark Zandi

of the research firm Moody's Economy.com predicted a "crash" of double-digit depreciation in some U.S. cities by 2007–2009.

Dean Baker

of the Center for Economic and Policy Research

was the first economist to identify the housing bubble, in a report in the summer of 2002.

The booming housing market halted abruptly in many parts of the U.S. in late summer of 2005, and as of summer 2006, several markets faced the issues of ballooning inventories, falling prices, and sharply reduced sales volumes. In August 2006, Barron's magazine warned, "a housing crisis approaches", and noted that the median price of new homes dropped almost 3% since January 2006, that new-home inventories hit a record in April and remained near all-time highs, that existing-home inventories were 39% higher than they were just one year earlier, and that sales were down more than 10%, and predicted that "the national median price of housing will probably fall by close to 30% in the next three years ... simple reversion to the mean." Fortune magazine labeled many previously strong housing markets as "Dead Zones;" other areas were classified as "Danger Zones" and "Safe Havens." Fortune also dispelled "four myths about the future of home prices." In Boston

The booming housing market halted abruptly in many parts of the U.S. in late summer of 2005, and as of summer 2006, several markets faced the issues of ballooning inventories, falling prices, and sharply reduced sales volumes. In August 2006, Barron's magazine warned, "a housing crisis approaches", and noted that the median price of new homes dropped almost 3% since January 2006, that new-home inventories hit a record in April and remained near all-time highs, that existing-home inventories were 39% higher than they were just one year earlier, and that sales were down more than 10%, and predicted that "the national median price of housing will probably fall by close to 30% in the next three years ... simple reversion to the mean." Fortune magazine labeled many previously strong housing markets as "Dead Zones;" other areas were classified as "Danger Zones" and "Safe Havens." Fortune also dispelled "four myths about the future of home prices." In Boston

, year-over-year prices dropped, sales fell, inventory increased, foreclosures were up, and the correction in Massachusetts

was called a "hard landing".

The previously booming housing markets in Washington, D.C.

, San Diego, California

, Phoenix, Arizona

, and other cities stalled as well. Searching the Arizona Regional Multiple Listing Service

(ARMLS) shows that in summer 2006, the for-sale housing inventory in Phoenix has grown to over 50,000 homes, of which nearly half are vacant (see graphic). Several home builders revised their forecasts sharply downward during summer 2006, e.g., D.R. Horton cut its yearly earnings forecast by one-third in July 2006, the value of luxury home builder Toll Brothers

' stock fell 50% between August 2005 and August 2006, and the Dow Jones U.S. Home Construction Index was down over 40% as of mid-August 2006. CEO Robert Toll of Toll Brothers

explained, "builders that built speculative homes are trying to move them by offering large incentives and discounts; and some sdate = 22 August 2006 | url=http://www.marketwatch.com/tools/quotanxious buyers are canceling contracts for homes already being built." Homebuilder Kara Homes announced on 13 September 2006 the "two most profitable quarters in the history of our company", yet filed for bankruptcy protection less than one month later on 6 October. Six months later on 10 April 2007, Kara Homes sold unfinished developments, causing prospective buyers from the previous year to lose deposits, some of whom put down more than $100,000.

As the housing market began to soften from winter 2005 through summer 2006, NAR

chief economist David Lereah

predicted a "soft landing" for the market. However, based on unprecedented rises in inventory and a sharply slowing market throughout 2006, Leslie Appleton-Young, the chief economist of the California Association of Realtors, said that she was not comfortable with the mild term "soft landing" to describe what was actually happening in California's real estate market. The Financial Times

warned of the impact on the U.S. economy

of the "hard edge" in the "soft landing" scenario, saying "A slowdown in these red-hot markets is inevitable. It may be gentle, but it is impossible to rule out a collapse of sentiment and of prices. ... If housing wealth stops rising ... the effect on the world's economy could be depressing indeed."

"It would be difficult to characterize the position of home builders as other than in a hard landing", said Robert Toll, CEO of Toll Brothers

. Angelo Mozilo, CEO of Countrywide Financial

, said "I've never seen a soft-landing in 53 years, so we have a ways to go before this levels out. I have to prepare the company for the worst that can happen." Following these reports, Lereah admitted that "he expects home prices to come down 5% nationally", and said that some cities in Florida

and California

could have "hard landings." National home sales and prices both fell dramatically again in March 2007 according to NAR

data, with sales down 13% to 482,000 from the peak of 554,000 in March 2006 and the national median price falling nearly 6% to $217,000 from the peak of $230,200 in July 2006. The plunge in existing-home sales was the steepest since 1989. The new home market also suffered. The biggest year over year drop in median home prices since 1970 occurred in April 2007. Median prices for new homes fell 10.9 percent according to the Commerce Department.

Based on slumping sales and prices in August 2006, economist Nouriel Roubini

warned that the housing sector was in "free fall" and would derail the rest of the economy, causing a recession

in 2007. Joseph Stiglitz, winner of the Nobel Prize in economics in 2001, agreed, saying that the U.S. might enter a recession

as house prices declined. The extent to which the economic slowdown, or possible recession, would last depended in large part on the resiliency of the U.S. consumer spending, which made up approximately 70% of the US$13.7 trillion economy. The evaporation of the wealth effect amid the current housing downturn could negatively affect the consumer confidence and provide further headwind for the U.S. economy and that of the rest of the world. The World Bank

lowered the global economic growth rate due to a housing slowdown in the United States, but it did not believe that the U.S. housing malaise would further spread to the rest of the world. The Fed chairman Benjamin Bernanke said in October 2006 that there was currently a "substantial correction" going on in the housing market and that the decline of residential housing construction was one of the "major drags that is causing the economy to slow"; he predicted that the correcting market would decrease U.S. economic growth by about one percent in the second half of 2006 and remain a drag on expansion into 2007.

Others speculated on the negative impact of the retirement of the Baby Boom

generation and the relative cost to rent on the declining housing market. In many parts of the United States, it was significantly cheaper to rent the same property than to purchase it; the national median

mortgage payment is $1,687 per month, nearly twice the median

rent payment of $868 per month.

, year-over-year prices were dropping, sales were falling, inventory was increasing, foreclosures were up, and the correction in Massachusetts

was termed a "hard landing".

The previously booming housing markets in Washington, D.C., San Diego

, Phoenix

and other cities were also stalled. A search through the Arizona Regional Multiple Listing Service

(ARMLS) shows that by the summer of 2006 the for-sale housing inventory in Phoenix had grown to over 50,000 homes, of which nearly half were vacant (see graphic). Several home builders revised their forecasts sharply downward during summer 2006/ For instance, D.R. Horton cut its yearly earnings forecast by one-third in July 2006, the value of luxury home builder Toll Brothers

' stock fell 50% between August 2005 and August 2006, and the Dow Jones U.S. Home Construction Index was down over 40% as of mid-August 2006. CEO Robert Toll of Toll Brothers

explained: "Builders that built speculative homes are trying to move them by offering large incentives and discounts; and some anxious buyers are canceling contracts for homes already being built." Homebuilder Kara Homes announced on September 13, 2006 the "two most profitable quarters in the history of our company", but filed for bankruptcy protection less than one month later on 6 October. Six months later on April 10, 2007, Kara Homes sold its unfinished developments, causing prospective buyers from the previous year, some of whom had put down more than $100,000, to lose their deposits.

As the housing market began to soften between the winter of 2005 and the summer of 2006, NAR

chief economist David Lereah

predicted a "soft landing" for the market. However, because of the unprecedented rises in inventory and a sharply slowing market throughout 2006, Leslie Appleton-Young, the chief economist of the California Association of Realtors, said that she was not comfortable with the mild term "soft landing" to describe what was actually happening in California's real estate market. The Financial Times

warned of the impact on the U.S. economy

of the "hard edge" in the "soft landing" scenario, saying that "A slowdown in these red-hot markets is inevitable. It may be gentle, but it is impossible to rule out a collapse of sentiment and of prices... If housing wealth stops rising... the effect on the world's economy could be depressing indeed."

"It would be difficult to characterize the position of home builders as other than in a hard landing", said Robert Toll, CEO of Toll Brothers

. Angelo Mozilo, CEO of Countrywide Financial

, said "I've never seen a soft landing in 53 years, so we have a ways to go before this levels out. I have to prepare the company for the worst that can happen." Following these reports, Lereah admitted that he expected "home prices to come down 5% nationally", and said that some cities in Florida and California could have "hard landings." National home sales and prices both saw further dramatic falls in March 2007, according to NAR

data, with sales down 13% to 482,000 from the peak of 554,000 in March 2006, and with the national median price falling nearly 6% to $217,000 from the peak of $230,200 in July 2006 . The plunge in existing-home sales was the steepest since 1989. The new home market was also suffering. The biggest year-over-year drop in median home prices since 1970 was reported in April 2007. Median prices for new homes fell 10.9%, according to the Commerce Department.

In August 2006, slumping sales and prices caused economist Nouriel Roubini

to warn that the housing sector was in "free fall" and would derail the rest of the economy, causing a recession

in 2007. Joseph Stiglitz, the 2001 winner of the Nobel Prize in economics, agreed, saying that the U.S. could enter a recession

as house prices declined. The duration of the economic slowdown or recession will depend in large part on the resiliency of U.S. consumer spending, which now makes up approximately 70% of the U.S. $13.7 trillion economy. The evaporation of the wealth effect amid the current housing downturn could negatively affect the consumer confidence and produce further headwinds for the economies of both the U.S. and the rest of the world. The World Bank

lowered its figures for the global economic growth rate due to the housing slowdown in the United States, but did not believe that the U.S. housing malaise would further spread to the rest of the world. The Fed chairman Benjamin Bernanke said in October 2006 that there was currently a "substantial correction" going on in the housing market, and that the decline of residential housing construction was one of the "major drags that is causing the economy to slow"; he predicted that the correcting market would decrease U.S. economic growth by about one per cent in the second half of 2006, and would continue to be a drag on expansion into 2007. The White House Council of Economic Advisers lowered its forecast for U.S. economic growth in 2008 from 3.1 per cent to 2.7 per cent and forecast higher unemployment, reflecting the turmoil in the credit and residential real-estate markets. The Bush Administration economic advisers also revised their unemployment outlook and predicted the unemployment rate could rise slightly above 5 per cent, up from the prevailing unemployment rate of 4.6 per cent.

Others speculated on the negative impact on the declining housing market of the retirement of the Baby Boom

generation and the relative cost of renting. In many parts of the United States, it is significantly cheaper to rent a property than to purchase the same property; the national median

mortgage payment is $1,687 per month, nearly twice the median

rent of $868 per month. However, the appreciation of home prices in many parts of the country has lured many renters into becoming homeowners. But the appreciation of home values far exceeded the income growth of many of these

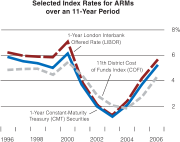

homebuyers, pushing them to leverage themselves beyond their means. They borrowed even more money in order to purchase homes whose cost was much greater than their ability to meet their mortgage obligations. Many of these homebuyers took out adjustable-rate mortgages during the period of low interest rates in order to purchase the home of their dreams. Initially, they were able to meet their mortgage obligations thanks to the low "teaser" rates being charged in the early years of the mortgage. However, as the Federal Reserve Bank applied its monetary contraction policy in 2005, many homeowners were stunned when their adjustable-rate mortgages began to reset to much higher rates in mid-2007 and their monthly payments jumped far above their ability to meet the monthly mortgage payments. Some homeowners began defaulting on their mortgages in mid-2007, and the cracks in the U.S. housing foundation became apparent.

mortgage industry collapsed due to higher-than-expected home foreclosure

rates, with more than 25 subprime lenders declaring bankruptcy, announcing significant losses, or putting themselves up for sale. The stock of the country's largest subprime lender, New Century Financial, plunged 84% amid Justice Department investigations, before ultimately filing for Chapter 11 bankruptcy on 2 April 2007 with liabilities exceeding $100 million. The manager of the world's largest bond fund PIMCO, warned in June 2007 that the subprime mortgage crisis

was not an isolated event and will eventually take a toll on the economy and whose ultimate impact will be on the impaired prices of homes. Bill Gross

, "a most reputable financial guru", sarcastically and ominously criticized the credit ratings

of the mortgage-based CDO

s now facing collapse:

Financial analysts predict that the subprime mortgage collapse will result in earnings reductions for large Wall Street

investment banks trading in mortgage-backed securities

, especially Bear Stearns

, Lehman Brothers

, Goldman Sachs

, Merrill Lynch

, and Morgan Stanley

. The solvency of two troubled hedge fund

s managed by Bear Stearns

was imperliled in June 2007 after Merrill Lynch

sold off assets seized from the funds and three other banks closed out their positions with them. The Bear Stearns funds once had over $20 billion of assets, but lost billions of dollars on securities backed by subprime mortgages. H&R Block

reported that it made a quarterly loss of $677 million on discontinued operations, which included subprime lender Option One, as well as writedowns, loss provisions on mortgage loans and the lower prices available for mortgages in the secondary market for mortgages. The units net asset value fell 21% to $1.1 billion as of April 30, 2007. The head of the mortgage industry consulting firm Wakefield Co. warned, "This is going to be a meltdown of unparalleled proportions. Billions will be lost." Bear Stearns

pledged up to US$3.2 billion in loans on 22 June 2007 to bail out one of its hedge funds that was collapsing because of bad bets on subprime mortgages. Peter Schiff

, president of Euro Pacific Capital, argued that if the bonds in the Bear Stearns

funds were auctioned on the open market, much weaker values would be plainly revealed. Schiff added, "This would force other hedge funds to similarly mark down the value of their holdings. Is it any wonder that Wall street is pulling out the stops to avoid such a catastrophe? ... Their true weakness will finally reveal the abyss into which the housing market is about to plummet." The New York Times

report connects this hedge fund crisis with lax lending standards: "The crisis this week from the near collapse of two hedge funds managed by Bear Stearns stems directly from the slumping housing market and the fallout from loose lending practices that showered money on people with weak, or subprime, credit, leaving many of them struggling to stay in their homes."

In the wake of the mortgage industry meltdown, Senator Chris Dodd, Chairman of the Banking Committee

held hearings in March 2007 and asked executives from the top five subprime mortgage companies to testify and explain their lending practices; Dodd said, "predatory lending practices" endangered the home ownership for millions of people. Moreover, Democratic senators such as Senator Charles Schumer

of New York are already proposing a federal government bailout of subprime borrowers in order to save homeowners from losing their residences. Opponents of such proposal assert that government bailout of subprime borrowers is not in the best interests of the U.S. economy because it will simply set a bad precedent, create a moral hazard, and worsen the speculation problem in the housing market. Lou Ranieri of Salomon Brothers

, inventor of the mortgage-backed securities

market in the 1970s, warned of the future impact of mortgage defaults: "This is the leading edge of the storm. ... If you think this is bad, imagine what it's going to be like in the middle of the crisis." In his opinion, more than $100 billion of home loans are likely to default when the problems in the subprime industry appear in the prime mortgage markets. Fed Chairman Alan Greenspan

praised the rise of the subprime mortgage industry and the tools with which it uses to assess credit-worthiness in an April 2005 speech:

(including "stated income" or "liar's loans" which are basically loans made to home buyers without the verification of borrowers' incomes; home buyers tend to overstate their incomes in order to get the loan amounts they desire to purchase their dream homes, thus called the "liar's loans") loans account for about 21 percent of loans outstanding and 39 percent of mortgages made in 2006. In April 2007, financial problems similar to the subprime mortgages began to appear with Alt-A loans made to homeowners who were thought to be less risky. American Home Mortgage

said that it would earn less and pay out a smaller dividend to its shareholders because it was being asked to buy back and write down the value of Alt-A loans made to borrowers with decent credit; causing company stocks to tumble 15.2 percent. The delinquency rate for Alt-A mortgages has been rising in 2007. In June 2007, Standard & Poor's

warned that U.S. homeowners with good credit are increasingly falling behind on mortgage payments, an indication that lenders have been offering higher risk loans outside the subprime market

; they said that rising late payments and defaults on Alt-A mortgages made in 2006 are "disconcerting" and delinquent borrowers appear to be "finding it increasingly difficult to refinance" or catch up on their payments. Late payments of at least 90 days and defaults on 2006 Alt-A mortgages have increased to 4.21 percent, up from 1.59 percent for 2005 mortgages and 0.81 percent for 2004, indicating that "subprime carnage is now spreading to near prime mortgages."

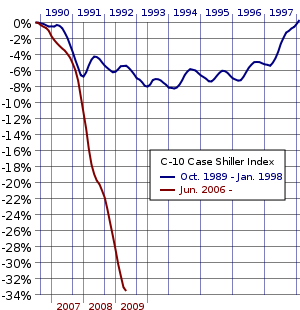

The 30-year mortgage rates increased by more than a half a percentage point to 6.74 percent during May–June 2007, affecting borrowers with the best credit just as a crackdown in subprime lending standards limits the pool of qualified buyers. The national median home price is poised for its first annual decline since the Great Depression

The 30-year mortgage rates increased by more than a half a percentage point to 6.74 percent during May–June 2007, affecting borrowers with the best credit just as a crackdown in subprime lending standards limits the pool of qualified buyers. The national median home price is poised for its first annual decline since the Great Depression

, and the NAR

reported that supply of unsold homes is at a record 4.2 million. Goldman Sachs

and Bear Stearns

, respectively the world's largest securities firm and largest underwriter of mortgage-backed securities in 2006, said in June 2007 that rising foreclosures reduced their earnings and the loss of billions from bad investments in the subprime market imperiled the solvency of several hedge fund

s. Mark Kiesel, executive vice president of a California-based Pacific Investment Management Co. said,

, that this process could take until 2014 or later.

Market trends

A market trend is a putative tendency of a financial market to move in a particular direction over time. These trends are classified as secular for long time frames, primary for medium time frames, and secondary for short time frames...

or "bubble bursting" of a United States housing bubble

United States housing bubble

The United States housing bubble is an economic bubble affecting many parts of the United States housing market in over half of American states. Housing prices peaked in early 2006, started to decline in 2006 and 2007, and may not yet have hit bottom as of 2011. On December 30, 2008 the...

; the most recent began following a national home price peak first identified in July 2006. Because realty trades in illiquid markets relative to financial assets such as common stock, timely valuation lags true values from three months to a year. Certain markets, including San Diego and Detroit, peaked as early as November 2005.

A real estate bubble

Real estate bubble

A real estate bubble or property bubble is a type of economic bubble that occurs periodically in local or global real estate markets...

is a type of economic bubble

Economic bubble

An economic bubble is "trade in high volumes at prices that are considerably at variance with intrinsic values"...

that occurs periodically in local, regional, national or global real estate

Real estate

In general use, esp. North American, 'real estate' is taken to mean "Property consisting of land and the buildings on it, along with its natural resources such as crops, minerals, or water; immovable property of this nature; an interest vested in this; an item of real property; buildings or...

markets. A housing bubble is characterized by rapid increases in the valuations

Real estate appraisal

Real estate appraisal, property valuation or land valuation is the process of valuing real property. The value usually sought is the property's Market Value. Appraisals are needed because compared to, say, corporate stock, real estate transactions occur very infrequently...

of real property

Real property

In English Common Law, real property, real estate, realty, or immovable property is any subset of land that has been legally defined and the improvements to it made by human efforts: any buildings, machinery, wells, dams, ponds, mines, canals, roads, various property rights, and so forth...

such as housing

House

A house is a building or structure that has the ability to be occupied for dwelling by human beings or other creatures. The term house includes many kinds of different dwellings ranging from rudimentary huts of nomadic tribes to free standing individual structures...

until unsustainable levels are reached relative to incomes, price-to-rent ratios, and other economic indicators of affordability. This in turn is followed by a market correction in which decreases in home prices can result in many owners holding negative equity

Negative equity

Negative equity occurs when the value of an asset used to secure a loan is less than the outstanding balance on the loan. In the United States, assets with negative equity are often referred to as being "underwater", and loans and borrowers with negative equity are said to be "upside down".People...

, a mortgage

Mortgage loan

A mortgage loan is a loan secured by real property through the use of a mortgage note which evidences the existence of the loan and the encumbrance of that realty through the granting of a mortgage which secures the loan...

debt higher than the value of the property.

Market correction predictions

|

Based on the historic trends in valuations of U.S. housing, many economists and business writers have predicted a market correction, ranging from a few percentage points, to 50% or more from peak values in some markets, and, in spite of the fact that this cooling has not affected all areas of the U.S., some have warned that it could and that the correction would be "nasty" and "severe". Chief economist Mark Zandi

Mark Zandi

Mark Zandi is an Iranian American economist and co-founder of Moody's Economy.com, a widely-cited source of economic analysis.. Moody's Economy.com is part of Moody's Analytics. Prior to founding Economy.com, Zandi was a regional economist at Chase Econometrics.He was born in Atlanta, Georgia of...

of the research firm Moody's Economy.com predicted a "crash" of double-digit depreciation in some U.S. cities by 2007–2009.

Dean Baker

Dean Baker

Dean Baker is an American macroeconomist and co-founder of the Center for Economic and Policy Research, with Mark Weisbrot. He previously was a senior economist at the Economic Policy Institute and an assistant professor of economics at Bucknell University. He has a Ph.D...

of the Center for Economic and Policy Research

Center for Economic and Policy Research

The Center for Economic and Policy Research is a progressive economic policy think-tank based in Washington, DC, founded in 1999. CEPR works on Social Security, the US housing bubble, developing country economies , and gaps in the social policy fabric of the US economy.According to its own...

was the first economist to identify the housing bubble, in a report in the summer of 2002.

Market weakness, 2005–2006

NAR National Association of Realtors The National Association of Realtors , whose members are known as Realtors, is North America's largest trade association. representing over 1.2 million members , including NAR's institutes, societies, and councils, involved in all aspects of the residential and commercial real estate industries... chief economist David Lereah David Lereah David Lereah is the President of , a real estate advisory and information company located in the Washington, DC area. Reecon Advisors is the owner and publisher of , one of the industry's leading Web sites providing intelligence and information on the residential real estate market. The Web site... 's Explanation of "What Happened" from the 2006 NAR National Association of Realtors The National Association of Realtors , whose members are known as Realtors, is North America's largest trade association. representing over 1.2 million members , including NAR's institutes, societies, and councils, involved in all aspects of the residential and commercial real estate industries... Leadership Conference

|

Boston

Boston is the capital of and largest city in Massachusetts, and is one of the oldest cities in the United States. The largest city in New England, Boston is regarded as the unofficial "Capital of New England" for its economic and cultural impact on the entire New England region. The city proper had...

, year-over-year prices dropped, sales fell, inventory increased, foreclosures were up, and the correction in Massachusetts

Massachusetts

The Commonwealth of Massachusetts is a state in the New England region of the northeastern United States of America. It is bordered by Rhode Island and Connecticut to the south, New York to the west, and Vermont and New Hampshire to the north; at its east lies the Atlantic Ocean. As of the 2010...

was called a "hard landing".

The previously booming housing markets in Washington, D.C.

Washington, D.C.

Washington, D.C., formally the District of Columbia and commonly referred to as Washington, "the District", or simply D.C., is the capital of the United States. On July 16, 1790, the United States Congress approved the creation of a permanent national capital as permitted by the U.S. Constitution....

, San Diego, California

San Diego, California

San Diego is the eighth-largest city in the United States and second-largest city in California. The city is located on the coast of the Pacific Ocean in Southern California, immediately adjacent to the Mexican border. The birthplace of California, San Diego is known for its mild year-round...

, Phoenix, Arizona

Phoenix, Arizona

Phoenix is the capital, and largest city, of the U.S. state of Arizona, as well as the sixth most populated city in the United States. Phoenix is home to 1,445,632 people according to the official 2010 U.S. Census Bureau data...

, and other cities stalled as well. Searching the Arizona Regional Multiple Listing Service

Multiple Listing Service

A multiple listing service is a suite of services that enables real estate brokers to establish contractual offers of compensation , facilitates cooperation with other broker participants, accumulates and disseminates information to enable appraisals, and is a facility for the orderly...

(ARMLS) shows that in summer 2006, the for-sale housing inventory in Phoenix has grown to over 50,000 homes, of which nearly half are vacant (see graphic). Several home builders revised their forecasts sharply downward during summer 2006, e.g., D.R. Horton cut its yearly earnings forecast by one-third in July 2006, the value of luxury home builder Toll Brothers

Toll Brothers

Toll Brothers is a Horsham, Pennsylvania based luxury homes builder.-Company Overview:Toll Brothers is a residential and commercial real estate development company with communities in 50 markets throughout 19 states...

' stock fell 50% between August 2005 and August 2006, and the Dow Jones U.S. Home Construction Index was down over 40% as of mid-August 2006. CEO Robert Toll of Toll Brothers

Toll Brothers

Toll Brothers is a Horsham, Pennsylvania based luxury homes builder.-Company Overview:Toll Brothers is a residential and commercial real estate development company with communities in 50 markets throughout 19 states...

explained, "builders that built speculative homes are trying to move them by offering large incentives and discounts; and some sdate = 22 August 2006 | url=http://www.marketwatch.com/tools/quotanxious buyers are canceling contracts for homes already being built." Homebuilder Kara Homes announced on 13 September 2006 the "two most profitable quarters in the history of our company", yet filed for bankruptcy protection less than one month later on 6 October. Six months later on 10 April 2007, Kara Homes sold unfinished developments, causing prospective buyers from the previous year to lose deposits, some of whom put down more than $100,000.

As the housing market began to soften from winter 2005 through summer 2006, NAR

National Association of Realtors

The National Association of Realtors , whose members are known as Realtors, is North America's largest trade association. representing over 1.2 million members , including NAR's institutes, societies, and councils, involved in all aspects of the residential and commercial real estate industries...

chief economist David Lereah

David Lereah

David Lereah is the President of , a real estate advisory and information company located in the Washington, DC area. Reecon Advisors is the owner and publisher of , one of the industry's leading Web sites providing intelligence and information on the residential real estate market. The Web site...

predicted a "soft landing" for the market. However, based on unprecedented rises in inventory and a sharply slowing market throughout 2006, Leslie Appleton-Young, the chief economist of the California Association of Realtors, said that she was not comfortable with the mild term "soft landing" to describe what was actually happening in California's real estate market. The Financial Times

Financial Times

The Financial Times is an international business newspaper. It is a morning daily newspaper published in London and printed in 24 cities around the world. Its primary rival is the Wall Street Journal, published in New York City....

warned of the impact on the U.S. economy

Economy of the United States

The economy of the United States is the world's largest national economy. Its nominal GDP was estimated to be nearly $14.5 trillion in 2010, approximately a quarter of nominal global GDP. The European Union has a larger collective economy, but is not a single nation...

of the "hard edge" in the "soft landing" scenario, saying "A slowdown in these red-hot markets is inevitable. It may be gentle, but it is impossible to rule out a collapse of sentiment and of prices. ... If housing wealth stops rising ... the effect on the world's economy could be depressing indeed."

"It would be difficult to characterize the position of home builders as other than in a hard landing", said Robert Toll, CEO of Toll Brothers

Toll Brothers

Toll Brothers is a Horsham, Pennsylvania based luxury homes builder.-Company Overview:Toll Brothers is a residential and commercial real estate development company with communities in 50 markets throughout 19 states...

. Angelo Mozilo, CEO of Countrywide Financial

Countrywide Financial

Bank of America Home Loans is the mortgage unit of Bank of America. Bank of America Home Loans is composed of:*Mortgage Banking, which originates purchases, securitizes, and services mortgages. In 2008, Bank of America purchased the failing Countrywide Financial for $4.1 billion...

, said "I've never seen a soft-landing in 53 years, so we have a ways to go before this levels out. I have to prepare the company for the worst that can happen." Following these reports, Lereah admitted that "he expects home prices to come down 5% nationally", and said that some cities in Florida

Florida

Florida is a state in the southeastern United States, located on the nation's Atlantic and Gulf coasts. It is bordered to the west by the Gulf of Mexico, to the north by Alabama and Georgia and to the east by the Atlantic Ocean. With a population of 18,801,310 as measured by the 2010 census, it...

and California

California

California is a state located on the West Coast of the United States. It is by far the most populous U.S. state, and the third-largest by land area...

could have "hard landings." National home sales and prices both fell dramatically again in March 2007 according to NAR

National Association of Realtors

The National Association of Realtors , whose members are known as Realtors, is North America's largest trade association. representing over 1.2 million members , including NAR's institutes, societies, and councils, involved in all aspects of the residential and commercial real estate industries...

data, with sales down 13% to 482,000 from the peak of 554,000 in March 2006 and the national median price falling nearly 6% to $217,000 from the peak of $230,200 in July 2006. The plunge in existing-home sales was the steepest since 1989. The new home market also suffered. The biggest year over year drop in median home prices since 1970 occurred in April 2007. Median prices for new homes fell 10.9 percent according to the Commerce Department.

Based on slumping sales and prices in August 2006, economist Nouriel Roubini

Nouriel Roubini

Nouriel Roubini is an American economist. He claims to have predicted both the collapse of the United States housing market and the worldwide recession which started in 2008. He teaches at New York University's Stern School of Business and is the chairman of Roubini Global Economics, an economic...

warned that the housing sector was in "free fall" and would derail the rest of the economy, causing a recession

Recession

In economics, a recession is a business cycle contraction, a general slowdown in economic activity. During recessions, many macroeconomic indicators vary in a similar way...

in 2007. Joseph Stiglitz, winner of the Nobel Prize in economics in 2001, agreed, saying that the U.S. might enter a recession

Recession

In economics, a recession is a business cycle contraction, a general slowdown in economic activity. During recessions, many macroeconomic indicators vary in a similar way...

as house prices declined. The extent to which the economic slowdown, or possible recession, would last depended in large part on the resiliency of the U.S. consumer spending, which made up approximately 70% of the US$13.7 trillion economy. The evaporation of the wealth effect amid the current housing downturn could negatively affect the consumer confidence and provide further headwind for the U.S. economy and that of the rest of the world. The World Bank

World Bank

The World Bank is an international financial institution that provides loans to developing countries for capital programmes.The World Bank's official goal is the reduction of poverty...

lowered the global economic growth rate due to a housing slowdown in the United States, but it did not believe that the U.S. housing malaise would further spread to the rest of the world. The Fed chairman Benjamin Bernanke said in October 2006 that there was currently a "substantial correction" going on in the housing market and that the decline of residential housing construction was one of the "major drags that is causing the economy to slow"; he predicted that the correcting market would decrease U.S. economic growth by about one percent in the second half of 2006 and remain a drag on expansion into 2007.

Others speculated on the negative impact of the retirement of the Baby Boom

Baby boom

A baby boom is any period marked by a greatly increased birth rate. This demographic phenomenon is usually ascribed within certain geographical bounds and when the number of annual births exceeds 2 per 100 women...

generation and the relative cost to rent on the declining housing market. In many parts of the United States, it was significantly cheaper to rent the same property than to purchase it; the national median

Median

In probability theory and statistics, a median is described as the numerical value separating the higher half of a sample, a population, or a probability distribution, from the lower half. The median of a finite list of numbers can be found by arranging all the observations from lowest value to...

mortgage payment is $1,687 per month, nearly twice the median

Median

In probability theory and statistics, a median is described as the numerical value separating the higher half of a sample, a population, or a probability distribution, from the lower half. The median of a finite list of numbers can be found by arranging all the observations from lowest value to...

rent payment of $868 per month.

The bursting of the bubble

The booming housing market appears to have halted abruptly in many parts of the U.S. in the late summer of 2005, and by the summer of 2006 several markets were facing the issues of ballooning inventories, falling prices and sharply reduced sales volumes. In August 2006, Barron's magazine warned that "a housing crisis approaches", and noted that the median price of new homes had dropped almost 3% since January 2006; that new-home inventories hit a record in April 2006, and remained near all-time highs; that existing-home inventories were 39% higher than they had been just one year before; and that sales were down more than 10%. It also predicted that "the national median price of housing will probably fall by close to 30% in the next three years ... simple reversion to the mean." Fortune magazine labelled many previously strong housing markets as "Dead Zones;" it classified other areas as "Danger Zones" and "Safe Havens". Fortune also dispelled "four myths about the future of home prices." In BostonBoston

Boston is the capital of and largest city in Massachusetts, and is one of the oldest cities in the United States. The largest city in New England, Boston is regarded as the unofficial "Capital of New England" for its economic and cultural impact on the entire New England region. The city proper had...

, year-over-year prices were dropping, sales were falling, inventory was increasing, foreclosures were up, and the correction in Massachusetts

Massachusetts

The Commonwealth of Massachusetts is a state in the New England region of the northeastern United States of America. It is bordered by Rhode Island and Connecticut to the south, New York to the west, and Vermont and New Hampshire to the north; at its east lies the Atlantic Ocean. As of the 2010...

was termed a "hard landing".

The previously booming housing markets in Washington, D.C., San Diego

San Diego, California

San Diego is the eighth-largest city in the United States and second-largest city in California. The city is located on the coast of the Pacific Ocean in Southern California, immediately adjacent to the Mexican border. The birthplace of California, San Diego is known for its mild year-round...

, Phoenix

Phoenix, Arizona

Phoenix is the capital, and largest city, of the U.S. state of Arizona, as well as the sixth most populated city in the United States. Phoenix is home to 1,445,632 people according to the official 2010 U.S. Census Bureau data...

and other cities were also stalled. A search through the Arizona Regional Multiple Listing Service

Multiple Listing Service

A multiple listing service is a suite of services that enables real estate brokers to establish contractual offers of compensation , facilitates cooperation with other broker participants, accumulates and disseminates information to enable appraisals, and is a facility for the orderly...

(ARMLS) shows that by the summer of 2006 the for-sale housing inventory in Phoenix had grown to over 50,000 homes, of which nearly half were vacant (see graphic). Several home builders revised their forecasts sharply downward during summer 2006/ For instance, D.R. Horton cut its yearly earnings forecast by one-third in July 2006, the value of luxury home builder Toll Brothers

Toll Brothers

Toll Brothers is a Horsham, Pennsylvania based luxury homes builder.-Company Overview:Toll Brothers is a residential and commercial real estate development company with communities in 50 markets throughout 19 states...

' stock fell 50% between August 2005 and August 2006, and the Dow Jones U.S. Home Construction Index was down over 40% as of mid-August 2006. CEO Robert Toll of Toll Brothers

Toll Brothers

Toll Brothers is a Horsham, Pennsylvania based luxury homes builder.-Company Overview:Toll Brothers is a residential and commercial real estate development company with communities in 50 markets throughout 19 states...

explained: "Builders that built speculative homes are trying to move them by offering large incentives and discounts; and some anxious buyers are canceling contracts for homes already being built." Homebuilder Kara Homes announced on September 13, 2006 the "two most profitable quarters in the history of our company", but filed for bankruptcy protection less than one month later on 6 October. Six months later on April 10, 2007, Kara Homes sold its unfinished developments, causing prospective buyers from the previous year, some of whom had put down more than $100,000, to lose their deposits.

As the housing market began to soften between the winter of 2005 and the summer of 2006, NAR

National Association of Realtors

The National Association of Realtors , whose members are known as Realtors, is North America's largest trade association. representing over 1.2 million members , including NAR's institutes, societies, and councils, involved in all aspects of the residential and commercial real estate industries...

chief economist David Lereah

David Lereah

David Lereah is the President of , a real estate advisory and information company located in the Washington, DC area. Reecon Advisors is the owner and publisher of , one of the industry's leading Web sites providing intelligence and information on the residential real estate market. The Web site...

predicted a "soft landing" for the market. However, because of the unprecedented rises in inventory and a sharply slowing market throughout 2006, Leslie Appleton-Young, the chief economist of the California Association of Realtors, said that she was not comfortable with the mild term "soft landing" to describe what was actually happening in California's real estate market. The Financial Times

Financial Times

The Financial Times is an international business newspaper. It is a morning daily newspaper published in London and printed in 24 cities around the world. Its primary rival is the Wall Street Journal, published in New York City....

warned of the impact on the U.S. economy

Economy of the United States

The economy of the United States is the world's largest national economy. Its nominal GDP was estimated to be nearly $14.5 trillion in 2010, approximately a quarter of nominal global GDP. The European Union has a larger collective economy, but is not a single nation...

of the "hard edge" in the "soft landing" scenario, saying that "A slowdown in these red-hot markets is inevitable. It may be gentle, but it is impossible to rule out a collapse of sentiment and of prices... If housing wealth stops rising... the effect on the world's economy could be depressing indeed."

"It would be difficult to characterize the position of home builders as other than in a hard landing", said Robert Toll, CEO of Toll Brothers

Toll Brothers

Toll Brothers is a Horsham, Pennsylvania based luxury homes builder.-Company Overview:Toll Brothers is a residential and commercial real estate development company with communities in 50 markets throughout 19 states...

. Angelo Mozilo, CEO of Countrywide Financial

Countrywide Financial

Bank of America Home Loans is the mortgage unit of Bank of America. Bank of America Home Loans is composed of:*Mortgage Banking, which originates purchases, securitizes, and services mortgages. In 2008, Bank of America purchased the failing Countrywide Financial for $4.1 billion...

, said "I've never seen a soft landing in 53 years, so we have a ways to go before this levels out. I have to prepare the company for the worst that can happen." Following these reports, Lereah admitted that he expected "home prices to come down 5% nationally", and said that some cities in Florida and California could have "hard landings." National home sales and prices both saw further dramatic falls in March 2007, according to NAR

National Association of Realtors

The National Association of Realtors , whose members are known as Realtors, is North America's largest trade association. representing over 1.2 million members , including NAR's institutes, societies, and councils, involved in all aspects of the residential and commercial real estate industries...

data, with sales down 13% to 482,000 from the peak of 554,000 in March 2006, and with the national median price falling nearly 6% to $217,000 from the peak of $230,200 in July 2006 . The plunge in existing-home sales was the steepest since 1989. The new home market was also suffering. The biggest year-over-year drop in median home prices since 1970 was reported in April 2007. Median prices for new homes fell 10.9%, according to the Commerce Department.

In August 2006, slumping sales and prices caused economist Nouriel Roubini

Nouriel Roubini

Nouriel Roubini is an American economist. He claims to have predicted both the collapse of the United States housing market and the worldwide recession which started in 2008. He teaches at New York University's Stern School of Business and is the chairman of Roubini Global Economics, an economic...

to warn that the housing sector was in "free fall" and would derail the rest of the economy, causing a recession

Recession

In economics, a recession is a business cycle contraction, a general slowdown in economic activity. During recessions, many macroeconomic indicators vary in a similar way...

in 2007. Joseph Stiglitz, the 2001 winner of the Nobel Prize in economics, agreed, saying that the U.S. could enter a recession

Recession

In economics, a recession is a business cycle contraction, a general slowdown in economic activity. During recessions, many macroeconomic indicators vary in a similar way...

as house prices declined. The duration of the economic slowdown or recession will depend in large part on the resiliency of U.S. consumer spending, which now makes up approximately 70% of the U.S. $13.7 trillion economy. The evaporation of the wealth effect amid the current housing downturn could negatively affect the consumer confidence and produce further headwinds for the economies of both the U.S. and the rest of the world. The World Bank

World Bank

The World Bank is an international financial institution that provides loans to developing countries for capital programmes.The World Bank's official goal is the reduction of poverty...

lowered its figures for the global economic growth rate due to the housing slowdown in the United States, but did not believe that the U.S. housing malaise would further spread to the rest of the world. The Fed chairman Benjamin Bernanke said in October 2006 that there was currently a "substantial correction" going on in the housing market, and that the decline of residential housing construction was one of the "major drags that is causing the economy to slow"; he predicted that the correcting market would decrease U.S. economic growth by about one per cent in the second half of 2006, and would continue to be a drag on expansion into 2007. The White House Council of Economic Advisers lowered its forecast for U.S. economic growth in 2008 from 3.1 per cent to 2.7 per cent and forecast higher unemployment, reflecting the turmoil in the credit and residential real-estate markets. The Bush Administration economic advisers also revised their unemployment outlook and predicted the unemployment rate could rise slightly above 5 per cent, up from the prevailing unemployment rate of 4.6 per cent.

Others speculated on the negative impact on the declining housing market of the retirement of the Baby Boom

Baby boom

A baby boom is any period marked by a greatly increased birth rate. This demographic phenomenon is usually ascribed within certain geographical bounds and when the number of annual births exceeds 2 per 100 women...

generation and the relative cost of renting. In many parts of the United States, it is significantly cheaper to rent a property than to purchase the same property; the national median

Median

In probability theory and statistics, a median is described as the numerical value separating the higher half of a sample, a population, or a probability distribution, from the lower half. The median of a finite list of numbers can be found by arranging all the observations from lowest value to...

mortgage payment is $1,687 per month, nearly twice the median

Median

In probability theory and statistics, a median is described as the numerical value separating the higher half of a sample, a population, or a probability distribution, from the lower half. The median of a finite list of numbers can be found by arranging all the observations from lowest value to...

rent of $868 per month. However, the appreciation of home prices in many parts of the country has lured many renters into becoming homeowners. But the appreciation of home values far exceeded the income growth of many of these

homebuyers, pushing them to leverage themselves beyond their means. They borrowed even more money in order to purchase homes whose cost was much greater than their ability to meet their mortgage obligations. Many of these homebuyers took out adjustable-rate mortgages during the period of low interest rates in order to purchase the home of their dreams. Initially, they were able to meet their mortgage obligations thanks to the low "teaser" rates being charged in the early years of the mortgage. However, as the Federal Reserve Bank applied its monetary contraction policy in 2005, many homeowners were stunned when their adjustable-rate mortgages began to reset to much higher rates in mid-2007 and their monthly payments jumped far above their ability to meet the monthly mortgage payments. Some homeowners began defaulting on their mortgages in mid-2007, and the cracks in the U.S. housing foundation became apparent.

Subprime mortgage industry collapse

In March 2007, the United States' subprimeSubprime lending

In finance, subprime lending means making loans to people who may have difficulty maintaining the repayment schedule...

mortgage industry collapsed due to higher-than-expected home foreclosure

Foreclosure

Foreclosure is the legal process by which a mortgage lender , or other lien holder, obtains a termination of a mortgage borrower 's equitable right of redemption, either by court order or by operation of law...

rates, with more than 25 subprime lenders declaring bankruptcy, announcing significant losses, or putting themselves up for sale. The stock of the country's largest subprime lender, New Century Financial, plunged 84% amid Justice Department investigations, before ultimately filing for Chapter 11 bankruptcy on 2 April 2007 with liabilities exceeding $100 million. The manager of the world's largest bond fund PIMCO, warned in June 2007 that the subprime mortgage crisis

Subprime mortgage crisis

The U.S. subprime mortgage crisis was one of the first indicators of the late-2000s financial crisis, characterized by a rise in subprime mortgage delinquencies and foreclosures, and the resulting decline of securities backed by said mortgages....

was not an isolated event and will eventually take a toll on the economy and whose ultimate impact will be on the impaired prices of homes. Bill Gross

Bill Gross

Bill Gross is an American businessman. Born in 1958, he grew up in Encino, California. He founded GNP Loudspeakers , an audio equipment manufacturer; GNP Development Inc., acquired by Lotus Software; and Knowledge Adventure, an educational software company, later acquired by Cendant...

, "a most reputable financial guru", sarcastically and ominously criticized the credit ratings

Moody's

Moody's Corporation is the holding company for Moody's Analytics and Moody's Investors Service, a credit rating agency which performs international financial research and analysis on commercial and government entities. The company also ranks the credit-worthiness of borrowers using a standardized...

of the mortgage-based CDO

Collateralized debt obligation

Collateralized debt obligations are a type of structured asset-backed security with multiple "tranches" that are issued by special purpose entities and collateralized by debt obligations including bonds and loans. Each tranche offers a varying degree of risk and return so as to meet investor demand...

s now facing collapse:

AAA? You were wooed Mr. Moody'sMoody'sMoody's Corporation is the holding company for Moody's Analytics and Moody's Investors Service, a credit rating agency which performs international financial research and analysis on commercial and government entities. The company also ranks the credit-worthiness of borrowers using a standardized...

and Mr. Poor'sStandard & Poor'sStandard & Poor's is a United States-based financial services company. It is a division of The McGraw-Hill Companies that publishes financial research and analysis on stocks and bonds. It is well known for its stock-market indices, the US-based S&P 500, the Australian S&P/ASX 200, the Canadian...

, by the makeup, those six-inch hooker heels, and a "tramp stamp." Many of these good looking girls are not high-class assets worth 100 cents on the dollar. ... And sorry Ben, but derivatives are a two-edged sword. Yes, they diversify risk and direct it away from the banking system into the eventual hands of unknown buyers, but they multiply leverage like the Andromeda strain. When interest rates go up, the Petri dish turns from a benign experiment in financial engineering to a destructive virus because the cost of that leverage ultimately reduces the price of assets. Houses anyone? ... AAAs? [T]he point is that there are hundreds of billions of dollars of this toxic waste and whether or not they're in CDOCollateralized debt obligationCollateralized debt obligations are a type of structured asset-backed security with multiple "tranches" that are issued by special purpose entities and collateralized by debt obligations including bonds and loans. Each tranche offers a varying degree of risk and return so as to meet investor demand...

s or Bear StearnsBear StearnsThe Bear Stearns Companies, Inc. based in New York City, was a global investment bank and securities trading and brokerage, until its sale to JPMorgan Chase in 2008 during the global financial crisis and recession...

hedge funds matters only to the extent of the timing of the unwind. [T]he subprime crisis is not an isolated event and it won't be contained by a few days of headlines in The New York TimesThe New York TimesThe New York Times is an American daily newspaper founded and continuously published in New York City since 1851. The New York Times has won 106 Pulitzer Prizes, the most of any news organization...

... The flaw lies in the homes that were financed with cheap and in some cases gratuitous money in 2004, 2005, and 2006. Because while the Bear hedge funds are now primarily history, those millions and millions of homes are not. They're not going anywhere ... except for their mortgages that is. Mortgage payments are going up, up, and up ... and so are delinquencies and defaults. A recent research piece by Bank of America estimates that approximately $500 billion of adjustable rate mortgages are scheduled to reset skyward in 2007 by an average of over 200 basis points. 2008 holds even more surprises with nearly $700 billion ARMS subject to reset, nearly ¾ of which are subprimes ... This problem—aided and abetted by Wall Street—ultimately resides in America's heartland, with millions and millions of overpriced homes and asset-backed collateral with a different address—Main Street.

Financial analysts predict that the subprime mortgage collapse will result in earnings reductions for large Wall Street

Wall Street

Wall Street refers to the financial district of New York City, named after and centered on the eight-block-long street running from Broadway to South Street on the East River in Lower Manhattan. Over time, the term has become a metonym for the financial markets of the United States as a whole, or...

investment banks trading in mortgage-backed securities

Mortgage-backed security

A mortgage-backed security is an asset-backed security that represents a claim on the cash flows from mortgage loans through a process known as securitization.-Securitization:...

, especially Bear Stearns

Bear Stearns

The Bear Stearns Companies, Inc. based in New York City, was a global investment bank and securities trading and brokerage, until its sale to JPMorgan Chase in 2008 during the global financial crisis and recession...

, Lehman Brothers

Lehman Brothers

Lehman Brothers Holdings Inc. was a global financial services firm. Before declaring bankruptcy in 2008, Lehman was the fourth largest investment bank in the USA , doing business in investment banking, equity and fixed-income sales and trading Lehman Brothers Holdings Inc. (former NYSE ticker...

, Goldman Sachs

Goldman Sachs

The Goldman Sachs Group, Inc. is an American multinational bulge bracket investment banking and securities firm that engages in global investment banking, securities, investment management, and other financial services primarily with institutional clients...

, Merrill Lynch

Merrill Lynch

Merrill Lynch is the wealth management division of Bank of America. With over 15,000 financial advisors and $2.2 trillion in client assets it is the world's largest brokerage. Formerly known as Merrill Lynch & Co., Inc., prior to 2009 the firm was publicly owned and traded on the New York...

, and Morgan Stanley

Morgan Stanley

Morgan Stanley is a global financial services firm headquartered in New York City serving a diversified group of corporations, governments, financial institutions, and individuals. Morgan Stanley also operates in 36 countries around the world, with over 600 offices and a workforce of over 60,000....

. The solvency of two troubled hedge fund

Hedge fund

A hedge fund is a private pool of capital actively managed by an investment adviser. Hedge funds are only open for investment to a limited number of accredited or qualified investors who meet criteria set by regulators. These investors can be institutions, such as pension funds, university...

s managed by Bear Stearns

Bear Stearns

The Bear Stearns Companies, Inc. based in New York City, was a global investment bank and securities trading and brokerage, until its sale to JPMorgan Chase in 2008 during the global financial crisis and recession...

was imperliled in June 2007 after Merrill Lynch

Merrill Lynch

Merrill Lynch is the wealth management division of Bank of America. With over 15,000 financial advisors and $2.2 trillion in client assets it is the world's largest brokerage. Formerly known as Merrill Lynch & Co., Inc., prior to 2009 the firm was publicly owned and traded on the New York...

sold off assets seized from the funds and three other banks closed out their positions with them. The Bear Stearns funds once had over $20 billion of assets, but lost billions of dollars on securities backed by subprime mortgages. H&R Block

H&R Block

H&R Block is a tax preparation company in the United States, claiming more than 22 million customers worldwide, with offices in Canada, Australia and the United Kingdom. The Kansas City-based company also offers banking, personal finance and business consulting services.Founded in 1955 by brothers...

reported that it made a quarterly loss of $677 million on discontinued operations, which included subprime lender Option One, as well as writedowns, loss provisions on mortgage loans and the lower prices available for mortgages in the secondary market for mortgages. The units net asset value fell 21% to $1.1 billion as of April 30, 2007. The head of the mortgage industry consulting firm Wakefield Co. warned, "This is going to be a meltdown of unparalleled proportions. Billions will be lost." Bear Stearns

Bear Stearns

The Bear Stearns Companies, Inc. based in New York City, was a global investment bank and securities trading and brokerage, until its sale to JPMorgan Chase in 2008 during the global financial crisis and recession...

pledged up to US$3.2 billion in loans on 22 June 2007 to bail out one of its hedge funds that was collapsing because of bad bets on subprime mortgages. Peter Schiff

Peter Schiff

Peter David Schiff is an American investment broker, author and financial commentator. Schiff is CEO and chief global strategist of Euro Pacific Capital Inc., a broker-dealer based in Westport, Connecticut and CEO of Euro Pacific Precious Metals, LLC, a gold and silver dealer based in New York...

, president of Euro Pacific Capital, argued that if the bonds in the Bear Stearns

Bear Stearns

The Bear Stearns Companies, Inc. based in New York City, was a global investment bank and securities trading and brokerage, until its sale to JPMorgan Chase in 2008 during the global financial crisis and recession...

funds were auctioned on the open market, much weaker values would be plainly revealed. Schiff added, "This would force other hedge funds to similarly mark down the value of their holdings. Is it any wonder that Wall street is pulling out the stops to avoid such a catastrophe? ... Their true weakness will finally reveal the abyss into which the housing market is about to plummet." The New York Times

The New York Times

The New York Times is an American daily newspaper founded and continuously published in New York City since 1851. The New York Times has won 106 Pulitzer Prizes, the most of any news organization...

report connects this hedge fund crisis with lax lending standards: "The crisis this week from the near collapse of two hedge funds managed by Bear Stearns stems directly from the slumping housing market and the fallout from loose lending practices that showered money on people with weak, or subprime, credit, leaving many of them struggling to stay in their homes."

In the wake of the mortgage industry meltdown, Senator Chris Dodd, Chairman of the Banking Committee

United States Senate Committee on Banking, Housing, and Urban Affairs

The United States Senate Committee on Banking, Housing, and Urban Affairs has jurisdiction over matters related to: banks and banking, price controls, deposit insurance, export promotion and controls, federal monetary policy, financial aid to commerce and industry, issuance of redemption of notes,...

held hearings in March 2007 and asked executives from the top five subprime mortgage companies to testify and explain their lending practices; Dodd said, "predatory lending practices" endangered the home ownership for millions of people. Moreover, Democratic senators such as Senator Charles Schumer

Charles Schumer

Charles Ellis "Chuck" Schumer is the senior United States Senator from New York and a member of the Democratic Party. First elected in 1998, he defeated three-term Republican incumbent Al D'Amato by a margin of 55%–44%. He was easily re-elected in 2004 by a margin of 71%–24% and in 2010 by a...

of New York are already proposing a federal government bailout of subprime borrowers in order to save homeowners from losing their residences. Opponents of such proposal assert that government bailout of subprime borrowers is not in the best interests of the U.S. economy because it will simply set a bad precedent, create a moral hazard, and worsen the speculation problem in the housing market. Lou Ranieri of Salomon Brothers

Salomon Brothers

Salomon Brothers was a bulge bracket, Wall Street investment bank. Founded in 1910 by three brothers along with a clerk named Ben Levy, it remained a partnership until the early 1980s, when it was acquired by the commodity trading firm Phibro Corporation and then became Salomon Inc. Eventually...

, inventor of the mortgage-backed securities

Mortgage-backed security

A mortgage-backed security is an asset-backed security that represents a claim on the cash flows from mortgage loans through a process known as securitization.-Securitization:...

market in the 1970s, warned of the future impact of mortgage defaults: "This is the leading edge of the storm. ... If you think this is bad, imagine what it's going to be like in the middle of the crisis." In his opinion, more than $100 billion of home loans are likely to default when the problems in the subprime industry appear in the prime mortgage markets. Fed Chairman Alan Greenspan

Alan Greenspan

Alan Greenspan is an American economist who served as Chairman of the Federal Reserve of the United States from 1987 to 2006. He currently works as a private advisor and provides consulting for firms through his company, Greenspan Associates LLC...

praised the rise of the subprime mortgage industry and the tools with which it uses to assess credit-worthiness in an April 2005 speech:

Innovation has brought about a multitude of new products, such as subprime loans and niche credit programs for immigrants. Such developments are representative of the market responses that have driven the financial services industry throughout the history of our country ... With these advances in technology, lenders have taken advantage of credit-scoring models and other techniques for efficiently extending credit to a broader spectrum of consumers. ... Where once more-marginal applicants would simply have been denied credit, lenders are now able to quite efficiently judge the risk posed by individual applicants and to price that risk appropriately. These improvements have led to rapid growth in subprime mortgage lending; indeed, today subprime mortgages account for roughly 10 percent of the number of all mortgages outstanding, up from just 1 or 2 percent in the early 1990s.Because of these remarks, along with his encouragement for the use of adjustable-rate mortgages, Greenspan has been criticized for his role in the rise of the housing bubble and the subsequent problems in the mortgage industry.

Alt-A mortgage problems

Subprime and Alt-AAlt-A

An Alt-A mortgage, short for Alternative A-paper, is a type of U.S. mortgage that, for various reasons, is considered riskier than A-paper, or "prime", and less risky than "subprime," the riskiest category. Alt-A interest rates, which are determined by credit risk, therefore tend to be between...

(including "stated income" or "liar's loans" which are basically loans made to home buyers without the verification of borrowers' incomes; home buyers tend to overstate their incomes in order to get the loan amounts they desire to purchase their dream homes, thus called the "liar's loans") loans account for about 21 percent of loans outstanding and 39 percent of mortgages made in 2006. In April 2007, financial problems similar to the subprime mortgages began to appear with Alt-A loans made to homeowners who were thought to be less risky. American Home Mortgage

American Home Mortgage

American Home Mortgage Investment Corporation was the 10th largest retail mortgage lender in the United States and was structured as a real estate investment trust .It has filed for bankruptcy....

said that it would earn less and pay out a smaller dividend to its shareholders because it was being asked to buy back and write down the value of Alt-A loans made to borrowers with decent credit; causing company stocks to tumble 15.2 percent. The delinquency rate for Alt-A mortgages has been rising in 2007. In June 2007, Standard & Poor's

Standard & Poor's

Standard & Poor's is a United States-based financial services company. It is a division of The McGraw-Hill Companies that publishes financial research and analysis on stocks and bonds. It is well known for its stock-market indices, the US-based S&P 500, the Australian S&P/ASX 200, the Canadian...

warned that U.S. homeowners with good credit are increasingly falling behind on mortgage payments, an indication that lenders have been offering higher risk loans outside the subprime market

Subprime lending

In finance, subprime lending means making loans to people who may have difficulty maintaining the repayment schedule...

; they said that rising late payments and defaults on Alt-A mortgages made in 2006 are "disconcerting" and delinquent borrowers appear to be "finding it increasingly difficult to refinance" or catch up on their payments. Late payments of at least 90 days and defaults on 2006 Alt-A mortgages have increased to 4.21 percent, up from 1.59 percent for 2005 mortgages and 0.81 percent for 2004, indicating that "subprime carnage is now spreading to near prime mortgages."

Foreclosure rates increase

Great Depression

The Great Depression was a severe worldwide economic depression in the decade preceding World War II. The timing of the Great Depression varied across nations, but in most countries it started in about 1929 and lasted until the late 1930s or early 1940s...

, and the NAR

National Association of Realtors

The National Association of Realtors , whose members are known as Realtors, is North America's largest trade association. representing over 1.2 million members , including NAR's institutes, societies, and councils, involved in all aspects of the residential and commercial real estate industries...

reported that supply of unsold homes is at a record 4.2 million. Goldman Sachs

Goldman Sachs

The Goldman Sachs Group, Inc. is an American multinational bulge bracket investment banking and securities firm that engages in global investment banking, securities, investment management, and other financial services primarily with institutional clients...

and Bear Stearns

Bear Stearns

The Bear Stearns Companies, Inc. based in New York City, was a global investment bank and securities trading and brokerage, until its sale to JPMorgan Chase in 2008 during the global financial crisis and recession...

, respectively the world's largest securities firm and largest underwriter of mortgage-backed securities in 2006, said in June 2007 that rising foreclosures reduced their earnings and the loss of billions from bad investments in the subprime market imperiled the solvency of several hedge fund

Hedge fund

A hedge fund is a private pool of capital actively managed by an investment adviser. Hedge funds are only open for investment to a limited number of accredited or qualified investors who meet criteria set by regulators. These investors can be institutions, such as pension funds, university...

s. Mark Kiesel, executive vice president of a California-based Pacific Investment Management Co. said,

It's a blood bath. ... We're talking about a two- to three-year downturn that will take a whole host of characters with it, from job creation to consumer confidence. Eventually it will take the stock market and corporate profit.According to Donald Burnette of Brightgreen Homeloans in Florida, one of the states hit hardest by the bursting housing bubble, the corresponding loss in equity from the drop in housing values has caused a new problems. "It is keeping even borrowers with good credit and solid resources from refinancing to much better terms. Even with tighter lending restrictions and the disappearance of subprime programs, there are many borrowers who would indeed qualify as "A" borrowers who can't refinance as they no longer have the equity in their homes that they had in 2005 or 2006. They will have to wait for the market to recover to refinance to the terms they deserve, and that could be years, or even a decade." It is foreseen, especially in California

California

California is a state located on the West Coast of the United States. It is by far the most populous U.S. state, and the third-largest by land area...

, that this process could take until 2014 or later.