Marginal tax rate

Encyclopedia

In a tax

system and in economics

, the tax rate describes the burden ratio

(usually expressed as a percentage

) at which a business or person is taxed. There are several methods used to present a tax rate: statutory, average, marginal, effective, effective average, and effective marginal. These rates can also be presented using different definitions applied to a tax base: inclusive and exclusive.

For an individual, it can be determined by increasing or decreasing the income earned or spent and calculating the change in taxes payable. An individual's tax bracket

is the range of income for which a given marginal tax rate applies. The marginal tax rate may increase or decrease as income or consumption increases, although in most countries the tax rate is (in principle) progressive. In such cases, the average tax rate will be lower than the marginal tax rate: an individual may have a marginal tax rate of 45%, but pay average tax of half this amount.

In a jurisdiction with a flat tax

on earnings, every taxpayer pays the same percentage of income, regardless of income or consumption. Some proponents of this system propose to exempt a fixed amount of earnings (such as the first $10,000) from the flat tax. In a revenue neutral situation in jurisdictions with progressive taxation regimes, where imposition of a "flat tax" would target neither an increase nor decrease in the total tax revenue, the net effect of the flat tax would be to shift a significant portion of the tax burden from wealthier tax brackets to less wealthy tax brackets.

In economics, marginal tax rates are important because they are one of the factors that determine incentives to increase income; at higher marginal tax rates, some argue, the individual has less incentive to earn more. This is the foundation of the Laffer curve

, which claims taxable income decreases as a function of marginal tax rate, and therefore tax revenue begins to decrease after a certain point.

Public discussion of "high taxes" may refer to overall tax rates or marginal taxes.

Marginal tax rates may be published explicitly, together with the corresponding tax brackets, but they can also be derived from published tax tables showing the tax for each income. It may be calculated noting how tax changes with changes in pre-tax income, rather than with taxable income.

Marginal tax rates do not fully describe the impact of taxation. A flat rate poll tax

has a marginal rate of zero, but a discontinuity in tax paid can lead to positively or negatively infinite marginal rates at particular points.

The effective tax rate is the amount of tax an individual or firm pays when all other government tax offsets or payments are applied, divided by the tax base (total income or spending). If certain groups have high degrees of tax offsets compared to other groups, their effective tax rate will be different, even where their official tax rates and marginal tax rates will be equal. The effective rate of tax can often be discussed in terms of the effective marginal rate of tax - namely the amount of effective tax paid as a percentage of the last dollar earned or spent.

Where social security

and other benefits are related to income, the combined tax and benefit effect can also be taken into account giving a result sometimes described as the marginal effective tax rate or the marginal deduction rate. If the marginal deduction rate exceeds 100%, then an increase in gross income leads to a decrease in disposable income, discouraging attempts to increase income. When this occurs for low income individuals, it is known as the "poverty trap

".

Tax rates can be presented differently due to differing definitions of tax base, which can make comparisons between tax systems confusing.

Tax rates can be presented differently due to differing definitions of tax base, which can make comparisons between tax systems confusing.

Some tax systems include the taxes owed in the tax base (tax-inclusive), while other tax systems do not include taxes owed as part of the base (tax-exclusive). In the United States

, sales tax

es are usually quoted exclusively and income tax

es are quoted inclusively. The majority of Europe, value added tax

(VAT) countries, include the tax amount when quoting merchandise prices, including Goods and Services Tax (GST) countries, such as Australia

and New Zealand

. However, those countries still define their tax rates on a tax exclusive basis.

For direct rate comparisons between exclusive and inclusive taxes, one rate must be manipulated to look like the other. When a tax system imposes taxes primarily on income

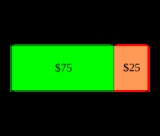

, the tax base is a household's pre-tax income. The appropriate income tax rate is applied to the tax base to calculate taxes owed. Under this formula, taxes to be paid are included in the base on which the tax rate is imposed. If an individual's gross income is $100 and income tax rate is 20%, taxes owed equals $20.

The income tax is taken "off the top", so the individual is left with $80 in after-tax money. Some tax laws impose taxes on a tax base equal to the pre-tax portion of a good's price. Unlike the income tax example above, these taxes do not include actual taxes owed as part of the base. A good priced at $80 with a 25% exclusive sales tax rate yields $20 in taxes owed. Since the sales tax is added "on the top", the individual pays $20 of tax on $80 of pre-tax goods for a total cost of $100. In either case, the tax base of $100 can be treated as two parts—$80 of after-tax spending money and $20 of taxes owed. A 25% exclusive tax rate approximates a 20% inclusive tax rate after adjustment. By including taxes owed in the tax base, an exclusive tax rate can be directly compared to an inclusive tax rate.

Tax

To tax is to impose a financial charge or other levy upon a taxpayer by a state or the functional equivalent of a state such that failure to pay is punishable by law. Taxes are also imposed by many subnational entities...

system and in economics

Economics

Economics is the social science that analyzes the production, distribution, and consumption of goods and services. The term economics comes from the Ancient Greek from + , hence "rules of the house"...

, the tax rate describes the burden ratio

Ratio

In mathematics, a ratio is a relationship between two numbers of the same kind , usually expressed as "a to b" or a:b, sometimes expressed arithmetically as a dimensionless quotient of the two which explicitly indicates how many times the first number contains the second In mathematics, a ratio is...

(usually expressed as a percentage

Percentage

In mathematics, a percentage is a way of expressing a number as a fraction of 100 . It is often denoted using the percent sign, “%”, or the abbreviation “pct”. For example, 45% is equal to 45/100, or 0.45.Percentages are used to express how large/small one quantity is, relative to another quantity...

) at which a business or person is taxed. There are several methods used to present a tax rate: statutory, average, marginal, effective, effective average, and effective marginal. These rates can also be presented using different definitions applied to a tax base: inclusive and exclusive.

Statutory

A statutory tax rate is the legally imposed rate. An income tax could have multiple statutory rates for different income levels, where a sales tax may have a flat statutory rate.Average

An average tax rate is the ratio of the amount of taxes paid to the tax base (taxable income or spending).- To calculate the average tax rate on an income tax, divide total tax liability by taxable income:

- Let

be the average tax rate.

be the average tax rate. - Let

be the tax liability.

be the tax liability. - Let

be the taxable income.

be the taxable income.

- Let

Marginal

A marginal tax rate is the tax rate that applies to the last dollar of the tax base (taxable income or spending), and is often applied to the change in one's tax obligation as income rises:- To calculate the marginal tax rate on an income tax:

- Let

be the marginal tax rate.

be the marginal tax rate. - Let

be the tax liability.

be the tax liability. - Let

be the taxable income.

be the taxable income.

- Let

For an individual, it can be determined by increasing or decreasing the income earned or spent and calculating the change in taxes payable. An individual's tax bracket

Tax bracket

Tax brackets are the divisions at which tax rates change in a progressive tax system . Essentially, they are the cutoff values for taxable income — income past a certain point will be taxed at a higher rate.-Example:Imagine that there are three tax brackets: 10%, 20%, and 30%...

is the range of income for which a given marginal tax rate applies. The marginal tax rate may increase or decrease as income or consumption increases, although in most countries the tax rate is (in principle) progressive. In such cases, the average tax rate will be lower than the marginal tax rate: an individual may have a marginal tax rate of 45%, but pay average tax of half this amount.

In a jurisdiction with a flat tax

Flat tax

A flat tax is a tax system with a constant marginal tax rate. Typically the term flat tax is applied in the context of an individual or corporate income that will be taxed at one marginal rate...

on earnings, every taxpayer pays the same percentage of income, regardless of income or consumption. Some proponents of this system propose to exempt a fixed amount of earnings (such as the first $10,000) from the flat tax. In a revenue neutral situation in jurisdictions with progressive taxation regimes, where imposition of a "flat tax" would target neither an increase nor decrease in the total tax revenue, the net effect of the flat tax would be to shift a significant portion of the tax burden from wealthier tax brackets to less wealthy tax brackets.

In economics, marginal tax rates are important because they are one of the factors that determine incentives to increase income; at higher marginal tax rates, some argue, the individual has less incentive to earn more. This is the foundation of the Laffer curve

Laffer curve

In economics, the Laffer curve is a theoretical representation of the relationship between government revenue raised by taxation and all possible rates of taxation. It is used to illustrate the concept of taxable income elasticity . The curve is constructed by thought experiment...

, which claims taxable income decreases as a function of marginal tax rate, and therefore tax revenue begins to decrease after a certain point.

Public discussion of "high taxes" may refer to overall tax rates or marginal taxes.

Marginal tax rates may be published explicitly, together with the corresponding tax brackets, but they can also be derived from published tax tables showing the tax for each income. It may be calculated noting how tax changes with changes in pre-tax income, rather than with taxable income.

Marginal tax rates do not fully describe the impact of taxation. A flat rate poll tax

Poll tax

A poll tax is a tax of a portioned, fixed amount per individual in accordance with the census . When a corvée is commuted for cash payment, in effect it becomes a poll tax...

has a marginal rate of zero, but a discontinuity in tax paid can lead to positively or negatively infinite marginal rates at particular points.

Effective

An effective tax rate refers to the actual rate, i.e., the rate existing in fact. Both average and marginal tax rates can be expressed as effective tax rates.The effective tax rate is the amount of tax an individual or firm pays when all other government tax offsets or payments are applied, divided by the tax base (total income or spending). If certain groups have high degrees of tax offsets compared to other groups, their effective tax rate will be different, even where their official tax rates and marginal tax rates will be equal. The effective rate of tax can often be discussed in terms of the effective marginal rate of tax - namely the amount of effective tax paid as a percentage of the last dollar earned or spent.

Effective average

An effective average tax rate (or average effective tax rate) may differ from an average tax rate because some measure of income other than taxable income is used. For example, the Joint Committee on Taxation typically calculates the effective average tax rate as the ratio of taxes paid to a constructed measure of "economic income".Effective marginal

An effective marginal tax rate (or marginal effective tax rate, marginal deduction rate) may differ from a marginal tax rate because the taxpayer may be in an income range in which she/he is subject to a phase-out of some exclusion or deduction.Where social security

Social security

Social security is primarily a social insurance program providing social protection or protection against socially recognized conditions, including poverty, old age, disability, unemployment and others. Social security may refer to:...

and other benefits are related to income, the combined tax and benefit effect can also be taken into account giving a result sometimes described as the marginal effective tax rate or the marginal deduction rate. If the marginal deduction rate exceeds 100%, then an increase in gross income leads to a decrease in disposable income, discouraging attempts to increase income. When this occurs for low income individuals, it is known as the "poverty trap

Welfare trap

The welfare trap theory asserts that taxation and welfare systems can jointly contribute to keep people on social insurance because the withdrawal of means tested benefits that comes with entering low-paid work causes there to be no significant increase in total income...

".

Inclusive/exclusive

Some tax systems include the taxes owed in the tax base (tax-inclusive), while other tax systems do not include taxes owed as part of the base (tax-exclusive). In the United States

United States

The United States of America is a federal constitutional republic comprising fifty states and a federal district...

, sales tax

Sales tax

A sales tax is a tax, usually paid by the consumer at the point of purchase, itemized separately from the base price, for certain goods and services. The tax amount is usually calculated by applying a percentage rate to the taxable price of a sale....

es are usually quoted exclusively and income tax

Income tax

An income tax is a tax levied on the income of individuals or businesses . Various income tax systems exist, with varying degrees of tax incidence. Income taxation can be progressive, proportional, or regressive. When the tax is levied on the income of companies, it is often called a corporate...

es are quoted inclusively. The majority of Europe, value added tax

Value added tax

A value added tax or value-added tax is a form of consumption tax. From the perspective of the buyer, it is a tax on the purchase price. From that of the seller, it is a tax only on the "value added" to a product, material or service, from an accounting point of view, by this stage of its...

(VAT) countries, include the tax amount when quoting merchandise prices, including Goods and Services Tax (GST) countries, such as Australia

Australia

Australia , officially the Commonwealth of Australia, is a country in the Southern Hemisphere comprising the mainland of the Australian continent, the island of Tasmania, and numerous smaller islands in the Indian and Pacific Oceans. It is the world's sixth-largest country by total area...

and New Zealand

New Zealand

New Zealand is an island country in the south-western Pacific Ocean comprising two main landmasses and numerous smaller islands. The country is situated some east of Australia across the Tasman Sea, and roughly south of the Pacific island nations of New Caledonia, Fiji, and Tonga...

. However, those countries still define their tax rates on a tax exclusive basis.

For direct rate comparisons between exclusive and inclusive taxes, one rate must be manipulated to look like the other. When a tax system imposes taxes primarily on income

Income

Income is the consumption and savings opportunity gained by an entity within a specified time frame, which is generally expressed in monetary terms. However, for households and individuals, "income is the sum of all the wages, salaries, profits, interests payments, rents and other forms of earnings...

, the tax base is a household's pre-tax income. The appropriate income tax rate is applied to the tax base to calculate taxes owed. Under this formula, taxes to be paid are included in the base on which the tax rate is imposed. If an individual's gross income is $100 and income tax rate is 20%, taxes owed equals $20.

The income tax is taken "off the top", so the individual is left with $80 in after-tax money. Some tax laws impose taxes on a tax base equal to the pre-tax portion of a good's price. Unlike the income tax example above, these taxes do not include actual taxes owed as part of the base. A good priced at $80 with a 25% exclusive sales tax rate yields $20 in taxes owed. Since the sales tax is added "on the top", the individual pays $20 of tax on $80 of pre-tax goods for a total cost of $100. In either case, the tax base of $100 can be treated as two parts—$80 of after-tax spending money and $20 of taxes owed. A 25% exclusive tax rate approximates a 20% inclusive tax rate after adjustment. By including taxes owed in the tax base, an exclusive tax rate can be directly compared to an inclusive tax rate.

- Inclusive income tax rate comparison to an exclusive sales tax rate:

- Let

be the income tax rate. For a 20% rate, then

be the income tax rate. For a 20% rate, then

- Let

be the rate in terms of a sales tax.

be the rate in terms of a sales tax. - Let

be the price of the good (including the tax).

be the price of the good (including the tax).

- Let

- The revenue that would go to the government:

- The revenue remaining for the seller of the good:

- To convert the tax, divide the money going to the government by the money the company nets:

- Therefore, to adjust any inclusive tax rate to that of an exclusive tax rate, divide the given rate by 1 minus that rate.

- 15% inclusive = 18% exclusive

- 20% inclusive = 25% exclusive

- 25% inclusive = 33% exclusive

- 33% inclusive = 50% exclusive

- 50% inclusive = 100% exclusive

See also

- Progressive taxProgressive taxA progressive tax is a tax by which the tax rate increases as the taxable base amount increases. "Progressive" describes a distribution effect on income or expenditure, referring to the way the rate progresses from low to high, where the average tax rate is less than the marginal tax rate...

- Proportional taxProportional taxA proportional tax is a tax imposed so that the tax rate is fixed. The amount of the tax is in proportion to the amount subject to taxation. "Proportional" describes a distribution effect on income or expenditure, referring to the way the rate remains consistent , where the marginal tax rate is...

- Regressive taxRegressive taxA regressive tax is a tax imposed in such a manner that the tax rate decreases as the amount subject to taxation increases. "Regressive" describes a distribution effect on income or expenditure, referring to the way the rate progresses from high to low, where the average tax rate exceeds the...

- Tax incidenceTax incidenceIn economics, tax incidence is the analysis of the effect of a particular tax on the distribution of economic welfare. Tax incidence is said to "fall" upon the group that, at the end of the day, bears the burden of the tax...

- Tax rates around the worldTax rates around the worldComparison of tax rates around the world is difficult and somewhat subjective. Tax laws in most countries are extremely complex, and tax burden falls differently on different groups in each country and sub-national unit. The graph below gives an indication by rank of some raw...

- List of countries by tax revenue as percentage of GDP

- Tax rates of EuropeTax rates of EuropeThis is a list of the maximum potential tax rates around Europe for certain income brackets. It is focused on three types of taxes: corporate and individual taxes and value added taxes...

- Tax exportingTax exportingTax exporting occurs when a country indirectly encourages economic activity to move to another country with a lower tax burden. This is more likely if the economic activity is more mobile....

- Capital flightCapital flightCapital flight, in economics, occurs when assets and/or money rapidly flow out of a country, due to an economic event and that disturbs investors and causes them to lower their valuation of the assets in that country, or otherwise to lose confidence in its economic...