Perfect competition

Overview

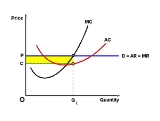

Market power

In economics, market power is the ability of a firm to alter the market price of a good or service. In perfectly competitive markets, market participants have no market power. A firm with market power can raise prices without losing its customers to competitors...

to set the price of a homogeneous product. Because the conditions for perfect competition are strict, there are few if any perfectly competitive markets. Still, buyers and sellers in some auction

Auction

An auction is a process of buying and selling goods or services by offering them up for bid, taking bids, and then selling the item to the highest bidder...

-type markets, say for commodities or some financial assets, may approximate the concept.

Unanswered Questions