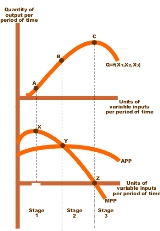

Production function

Overview

Microeconomics

Microeconomics is a branch of economics that studies the behavior of how the individual modern household and firms make decisions to allocate limited resources. Typically, it applies to markets where goods or services are being bought and sold...

and macroeconomics

Macroeconomics

Macroeconomics is a branch of economics dealing with the performance, structure, behavior, and decision-making of the whole economy. This includes a national, regional, or global economy...

, a production function is a function

Function (mathematics)

In mathematics, a function associates one quantity, the argument of the function, also known as the input, with another quantity, the value of the function, also known as the output. A function assigns exactly one output to each input. The argument and the value may be real numbers, but they can...

that specifies the output of a firm, an industry, or an entire economy for all combinations of inputs

Factors of production

In economics, factors of production means inputs and finished goods means output. Input determines the quantity of output i.e. output depends upon input. Input is the starting point and output is the end point of production process and such input-output relationship is called a production function...

. This function is an assumed technological relationship, based on the current state of engineering

Engineering

Engineering is the discipline, art, skill and profession of acquiring and applying scientific, mathematical, economic, social, and practical knowledge, in order to design and build structures, machines, devices, systems, materials and processes that safely realize improvements to the lives of...

knowledge; it does not represent the result of economic choices, but rather is an externally given entity that influences economic decision-making. Almost all economic theories presuppose a production function, either on the firm level or the aggregate level.

Unanswered Questions

Discussions