Cost-of-production theory of value

Encyclopedia

In economics

, the cost-of-production theory of value is the theory that the price of an object or condition is determined by the sum of the cost of the resources that went into making it. The cost can compose any of the factors of production

(including labor, capital, or land) and taxation

.

The theory makes the most sense under assumptions of constant returns to scale and the existence of just one non-produced factor of production. These are the assumptions of the so-called non-substitution theorem. Under these assumptions, the long run price of a commodity is equal to the sum of the cost of the inputs into that commodity, including interest charges.

. Piero Sraffa

, in his introduction to the first volume of the "Collected Works of David Ricardo", referred to Adam Smith's adding up theory. Smith contrasted natural prices

with market price

. Smith theorized that market prices would tend towards natural prices, where outputs would be at what he characterized as the "level of effectual demand". At this level, Smith's natural prices of commodities are the sum of the natural rates of wages, profits, and rent that must be paid for inputs into production. (Smith is ambiguous about whether rent is price-determining or price determined. The latter view is the consensus of later classical economists

, with the Ricardo-Malthus-West theory of rent.)

David Ricardo

mixed such cost of production theory of prices with the labor theory of value

, as that latter theory was understood by Eugen von Bohm-Bawerk

and others. This is the theory that prices tend toward proportionality to the socially necessary labor embodied in a commodity. Ricardo sets this theory at the start of the first chapter of his "Principles of Political Economy and Taxation". Ricardo also refutes the labor theory of value in later sections of that chapter. This refutation leads to what later became known as the transformation problem

. Karl Marx

later takes up that theory in the first volume of "Capital", while indicating that he is quite aware that the theory is untrue at lower levels of abstraction. This has led to all sorts of arguments over what both David Ricardo and Karl Marx "really meant". Nevertheless, it seems undeniable that all the major classical economics and Marx explicitly rejected the labor theory of price (http://links.jstor.org/sici?sici=0002-8282(195905)49%3A2%3C462%3AWWTLTO%3E2.0.CO%3B2-9).

A somewhat different theory of cost-determined prices is provided by the "neo-Ricardian school" of Piero Sraffa

and his followers.

The Polish economist Michał Kalecki http://cepa.newschool.edu/het/profiles/kalecki.htm distinguished between sectors with "cost-determined prices" (such as manufacturing and services) and those with "demand-determined prices" (such as agriculture and raw material extraction).

One might think of this theory as equivalent to modern theories of markup-pricing, full-cost pricing, or administrative pricing. Ever since Hall and Hitch, economists have found that the evidence gathered in surveys of businessmen support such theories.

Most contemporary economists accept neoclassical economics

or mainstream economics. The non-substitution theorem is presented in graduate level microeconomics textbooks as a theorem of mainstream economics. Also many mainstream economists think they can justify theories of full-cost pricing within their theory. The majority of mainstream economists would probably then accept this theory as an element in their theory which does not give adequate attention to issues of consumer demand and marginal utility

.

.

In economics, returns to scale and economies of scale are related terms that describe what happens as the scale of production increases. They are different terms and are not to be used interchangeably.

There are many different accounts of labor value, with the common element that the "value" of an exchangeable good or service is, or ought to be, or tends to be, or can be considered as, equal or proportional to the amount of labor required to produce it (including the labor required to produce the raw materials and machinery used in production).

Different labor theories of value prevailed amongst classical economists through to the mid-19th century. It is especially associated with Adam Smith and David Ricardo. Since that time it is most often associated with Marxian economics; while among modern mainstream economists it is considered to be superseded by the marginal utility approach.

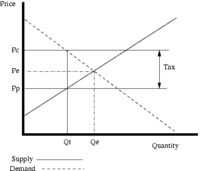

Tax

es and subsidies

change the price of goods and services. A marginal tax on the sellers of a good will shift the supply curve to the left until the vertical distance between the two supply curves is equal to the per unit tax; when other things remain equal, this will increase the price

paid by the consumers (which is equal to the new market price), and decrease the price received by the sellers. Marginal subsidies on production will shift the supply curve to the right until the vertical distance between the two supply curves is equal to the per unit subsidy; when other things remain equal, this will decrease price paid by the consumers (which is equal to the new market price) and increase the price received by the producers.

Economics

Economics is the social science that analyzes the production, distribution, and consumption of goods and services. The term economics comes from the Ancient Greek from + , hence "rules of the house"...

, the cost-of-production theory of value is the theory that the price of an object or condition is determined by the sum of the cost of the resources that went into making it. The cost can compose any of the factors of production

Factors of production

In economics, factors of production means inputs and finished goods means output. Input determines the quantity of output i.e. output depends upon input. Input is the starting point and output is the end point of production process and such input-output relationship is called a production function...

(including labor, capital, or land) and taxation

Effect of taxes and subsidies on price

Taxes and subsidies change the price of goods and, as a result, the quantity consumed.- Tax impact :A marginal tax on the sellers of a good will shift the supply curve to the left until the vertical distance between the two supply curves is equal to the per unit tax; when other things remain equal,...

.

The theory makes the most sense under assumptions of constant returns to scale and the existence of just one non-produced factor of production. These are the assumptions of the so-called non-substitution theorem. Under these assumptions, the long run price of a commodity is equal to the sum of the cost of the inputs into that commodity, including interest charges.

Historical development of theory

Historically, the most well known proponent of such theories is probably Adam SmithAdam Smith

Adam Smith was a Scottish social philosopher and a pioneer of political economy. One of the key figures of the Scottish Enlightenment, Smith is the author of The Theory of Moral Sentiments and An Inquiry into the Nature and Causes of the Wealth of Nations...

. Piero Sraffa

Piero Sraffa

Piero Sraffa was an influential Italian economist whose book Production of Commodities by Means of Commodities is taken as founding the Neo-Ricardian school of Economics.- Early life :...

, in his introduction to the first volume of the "Collected Works of David Ricardo", referred to Adam Smith's adding up theory. Smith contrasted natural prices

Prices of production

Prices of production refers to a concept in Karl Marx's critique of political economy. It is introduced in the third volume of Das Kapital, where Marx considers the operation of capitalist production as the unity of a production process and a circulation process involving commodities, money and...

with market price

Market price

In economics, market price is the economic price for which a good or service is offered in the marketplace. It is of interest mainly in the study of microeconomics...

. Smith theorized that market prices would tend towards natural prices, where outputs would be at what he characterized as the "level of effectual demand". At this level, Smith's natural prices of commodities are the sum of the natural rates of wages, profits, and rent that must be paid for inputs into production. (Smith is ambiguous about whether rent is price-determining or price determined. The latter view is the consensus of later classical economists

Classical economics

Classical economics is widely regarded as the first modern school of economic thought. Its major developers include Adam Smith, Jean-Baptiste Say, David Ricardo, Thomas Malthus and John Stuart Mill....

, with the Ricardo-Malthus-West theory of rent.)

David Ricardo

David Ricardo

David Ricardo was an English political economist, often credited with systematising economics, and was one of the most influential of the classical economists, along with Thomas Malthus, Adam Smith, and John Stuart Mill. He was also a member of Parliament, businessman, financier and speculator,...

mixed such cost of production theory of prices with the labor theory of value

Labor theory of value

The labor theories of value are heterodox economic theories of value which argue that the value of a commodity is related to the labor needed to produce or obtain that commodity. The concept is most often associated with Marxian economics...

, as that latter theory was understood by Eugen von Bohm-Bawerk

Eugen von Böhm-Bawerk

Eugen Ritter von Böhm-Bawerk was an Austrian economist who made important contributions to the development of the Austrian School of economics.-Biography:...

and others. This is the theory that prices tend toward proportionality to the socially necessary labor embodied in a commodity. Ricardo sets this theory at the start of the first chapter of his "Principles of Political Economy and Taxation". Ricardo also refutes the labor theory of value in later sections of that chapter. This refutation leads to what later became known as the transformation problem

Transformation problem

In 20th century discussions of Karl Marx's economics the transformation problem is the problem of finding a general rule to transform the "values" of commodities into the "competitive prices" of the marketplace...

. Karl Marx

Karl Marx

Karl Heinrich Marx was a German philosopher, economist, sociologist, historian, journalist, and revolutionary socialist. His ideas played a significant role in the development of social science and the socialist political movement...

later takes up that theory in the first volume of "Capital", while indicating that he is quite aware that the theory is untrue at lower levels of abstraction. This has led to all sorts of arguments over what both David Ricardo and Karl Marx "really meant". Nevertheless, it seems undeniable that all the major classical economics and Marx explicitly rejected the labor theory of price (http://links.jstor.org/sici?sici=0002-8282(195905)49%3A2%3C462%3AWWTLTO%3E2.0.CO%3B2-9).

A somewhat different theory of cost-determined prices is provided by the "neo-Ricardian school" of Piero Sraffa

Piero Sraffa

Piero Sraffa was an influential Italian economist whose book Production of Commodities by Means of Commodities is taken as founding the Neo-Ricardian school of Economics.- Early life :...

and his followers.

The Polish economist Michał Kalecki http://cepa.newschool.edu/het/profiles/kalecki.htm distinguished between sectors with "cost-determined prices" (such as manufacturing and services) and those with "demand-determined prices" (such as agriculture and raw material extraction).

One might think of this theory as equivalent to modern theories of markup-pricing, full-cost pricing, or administrative pricing. Ever since Hall and Hitch, economists have found that the evidence gathered in surveys of businessmen support such theories.

Most contemporary economists accept neoclassical economics

Neoclassical economics

Neoclassical economics is a term variously used for approaches to economics focusing on the determination of prices, outputs, and income distributions in markets through supply and demand, often mediated through a hypothesized maximization of utility by income-constrained individuals and of profits...

or mainstream economics. The non-substitution theorem is presented in graduate level microeconomics textbooks as a theorem of mainstream economics. Also many mainstream economists think they can justify theories of full-cost pricing within their theory. The majority of mainstream economists would probably then accept this theory as an element in their theory which does not give adequate attention to issues of consumer demand and marginal utility

Marginal utility

In economics, the marginal utility of a good or service is the utility gained from an increase in the consumption of that good or service...

.

Market price

Market price is an economic concept with commonplace familiarity; it is the price that a good or service is offered at, or will fetch, in the marketplace; it is of interest mainly in the study of microeconomics. Market value and market price are equal only under conditions of market efficiency, equilibrium, and rational expectationsRational expectations

Rational expectations is a hypothesis in economics which states that agents' predictions of the future value of economically relevant variables are not systematically wrong in that all errors are random. An alternative formulation is that rational expectations are model-consistent expectations, in...

.

In economics, returns to scale and economies of scale are related terms that describe what happens as the scale of production increases. They are different terms and are not to be used interchangeably.

Labor theory of value

The labor theories of value (LTV) are theories in economics according to which the true values of commodities are related to the labor needed to produce them.There are many different accounts of labor value, with the common element that the "value" of an exchangeable good or service is, or ought to be, or tends to be, or can be considered as, equal or proportional to the amount of labor required to produce it (including the labor required to produce the raw materials and machinery used in production).

Different labor theories of value prevailed amongst classical economists through to the mid-19th century. It is especially associated with Adam Smith and David Ricardo. Since that time it is most often associated with Marxian economics; while among modern mainstream economists it is considered to be superseded by the marginal utility approach.

Taxes and subsidies

Tax

Tax

To tax is to impose a financial charge or other levy upon a taxpayer by a state or the functional equivalent of a state such that failure to pay is punishable by law. Taxes are also imposed by many subnational entities...

es and subsidies

Subsidy

A subsidy is an assistance paid to a business or economic sector. Most subsidies are made by the government to producers or distributors in an industry to prevent the decline of that industry or an increase in the prices of its products or simply to encourage it to hire more labor A subsidy (also...

change the price of goods and services. A marginal tax on the sellers of a good will shift the supply curve to the left until the vertical distance between the two supply curves is equal to the per unit tax; when other things remain equal, this will increase the price

Price

-Definition:In ordinary usage, price is the quantity of payment or compensation given by one party to another in return for goods or services.In modern economies, prices are generally expressed in units of some form of currency...

paid by the consumers (which is equal to the new market price), and decrease the price received by the sellers. Marginal subsidies on production will shift the supply curve to the right until the vertical distance between the two supply curves is equal to the per unit subsidy; when other things remain equal, this will decrease price paid by the consumers (which is equal to the new market price) and increase the price received by the producers.

See also

- production, costs, and pricingProduction, costs, and pricingThe following outline is provided as an overview of and topical guide to industrial organization:Industrial organization – describes the behavior of firms in the marketplace with regard to production, pricing, employment and other decisions...

- list of economics topics

- prices of productionPrices of productionPrices of production refers to a concept in Karl Marx's critique of political economy. It is introduced in the third volume of Das Kapital, where Marx considers the operation of capitalist production as the unity of a production process and a circulation process involving commodities, money and...