Competitive equilibrium

Encyclopedia

Competitive market equilibrium is the traditional concept of economic equilibrium

, appropriate for the analysis of commodity markets with flexible prices and many traders, and serving as the benchmark of efficiency in economic analysis. It relies crucially on the assumption of a competitive environment where each trader decides upon a quantity that is so small compared to the total quantity traded in the market that their individual transactions have no influence on the prices. Competitive markets are an ideal, a standard that other market structures are evaluated by.

A competitive equilibrium is a vector of prices and an allocation such that given the prices, each trader by maximizing his objective function (profit, preferences) subject to his technological possibilities and resource constraints plans to trade into his part of the proposed allocation, and such that the prices make all net trades compatible with one another ('clear the market') by equating aggregate supply and demand for the commodities which are traded.

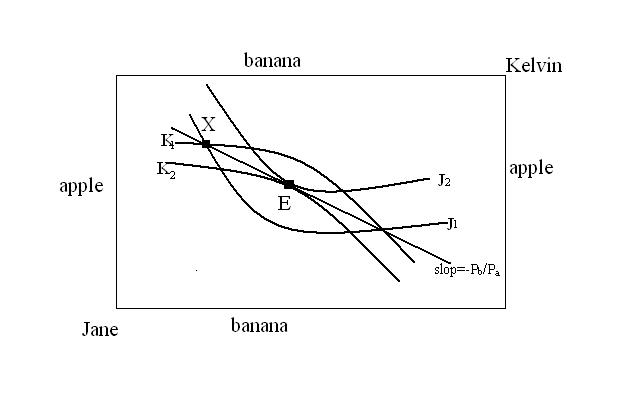

A simple example is a society where there are only 2 products, bananas and apples, and 2 individuals, Jane and Kelvin. The price of bananas is Pb, and the price of apples is Pa.

The indifference curves J1 of Jane and K1 of Kelvin first intersect at point X, where Jane has more apples than Kelvin does, Kelvin has more bananas than Jane does, and they are willing to trade with each other at the prices Pb and Pa. After trading both Jane and Kelvin move to an indifference curve which depicts a higher level of utility, J2 and K2. The new indifference curves intersect at point E. The slope of the tangent of both curves equals -Pb/Pa.

And the MRSJane=Pb/Pa;

MRSKelvin=Pb/Pa.

The marginal rate of substitution of Jane equals that of Kelvin. Therefore the 2 individuals society reaches Pareto efficiency

, where there is no way to make Jane or Kelvin better off without making the other worse off.

). By definition, this ensures allocative efficiency

(the additional value society places on another unit of the good is equal to what society must give up in resources to produce it).

Note that microeconomic analysis does NOT assume additive utility nor does it assume any interpersonal utility tradeoffs.

Efficiency therefore refers to the absence of Pareto improvements. It does not in any way opine on the fairness of the allocation (in the sense of distributive justice

or equity

). An 'efficient' equilibrium could be one where one player has all the goods and other players have none (in an extreme example). This is efficient in the sense that one may not be able to find a Pareto improvement - which makes all players (including the one with everything in this case) better off (for a strict Pareto improvement), or not worse off.

Economic equilibrium

In economics, economic equilibrium is a state of the world where economic forces are balanced and in the absence of external influences the values of economic variables will not change. It is the point at which quantity demanded and quantity supplied are equal...

, appropriate for the analysis of commodity markets with flexible prices and many traders, and serving as the benchmark of efficiency in economic analysis. It relies crucially on the assumption of a competitive environment where each trader decides upon a quantity that is so small compared to the total quantity traded in the market that their individual transactions have no influence on the prices. Competitive markets are an ideal, a standard that other market structures are evaluated by.

A competitive equilibrium is a vector of prices and an allocation such that given the prices, each trader by maximizing his objective function (profit, preferences) subject to his technological possibilities and resource constraints plans to trade into his part of the proposed allocation, and such that the prices make all net trades compatible with one another ('clear the market') by equating aggregate supply and demand for the commodities which are traded.

A simple example is a society where there are only 2 products, bananas and apples, and 2 individuals, Jane and Kelvin. The price of bananas is Pb, and the price of apples is Pa.

The indifference curves J1 of Jane and K1 of Kelvin first intersect at point X, where Jane has more apples than Kelvin does, Kelvin has more bananas than Jane does, and they are willing to trade with each other at the prices Pb and Pa. After trading both Jane and Kelvin move to an indifference curve which depicts a higher level of utility, J2 and K2. The new indifference curves intersect at point E. The slope of the tangent of both curves equals -Pb/Pa.

And the MRSJane=Pb/Pa;

MRSKelvin=Pb/Pa.

The marginal rate of substitution of Jane equals that of Kelvin. Therefore the 2 individuals society reaches Pareto efficiency

Pareto efficiency

Pareto efficiency, or Pareto optimality, is a concept in economics with applications in engineering and social sciences. The term is named after Vilfredo Pareto, an Italian economist who used the concept in his studies of economic efficiency and income distribution.Given an initial allocation of...

, where there is no way to make Jane or Kelvin better off without making the other worse off.

The competitive equilibrium and allocative efficiency

At the competitive equilibrium, the value society places on a good is equivalent to the value of the resources given up to produce it (marginal benefit equals marginal costMarginal cost

In economics and finance, marginal cost is the change in total cost that arises when the quantity produced changes by one unit. That is, it is the cost of producing one more unit of a good...

). By definition, this ensures allocative efficiency

Allocative efficiency

Allocative efficiency is a theoretical measure of the benefit or utility derived from a proposed or actual selection in the allocation or allotment of resources....

(the additional value society places on another unit of the good is equal to what society must give up in resources to produce it).

Note that microeconomic analysis does NOT assume additive utility nor does it assume any interpersonal utility tradeoffs.

Efficiency therefore refers to the absence of Pareto improvements. It does not in any way opine on the fairness of the allocation (in the sense of distributive justice

Distributive justice

Distributive justice concerns what some consider to be socially just allocation of goods in a society. A society in which incidental inequalities in outcome do not arise would be considered a society guided by the principles of distributive justice...

or equity

Equity (economics)

Equity is the concept or idea of fairness in economics, particularly as to taxation or welfare economics. More specifically it may refer to equal life chances regardless of identity, to provide all citizens with a basic minimum of income/goods/services or to increase funds and commitment for...

). An 'efficient' equilibrium could be one where one player has all the goods and other players have none (in an extreme example). This is efficient in the sense that one may not be able to find a Pareto improvement - which makes all players (including the one with everything in this case) better off (for a strict Pareto improvement), or not worse off.